Shifting economic winds are buffeting the Arizona economy. The labor market remains very tight, with low unemployment, high levels of labor market churn, and a mountain of open jobs. Retail sales have slowed but remain surprisingly resilient. At the same time, income gains are more than offset by inflation while rising mortgage interest rates and low affordability have combined to generate declining home sales, prices, and permit activity.

READ ALSO: Arizona property taxes will see No. 3 greatest 5-year increase

READ ALSO: Here’s the salary needed to buy a home in Phoenix

The baseline (most likely) forecast for the U.S. economy now includes a mild downturn beginning late this year and ending in mid-2023. That is expected to take the wind out of Arizona’s sails, generating a significant slowdown in growth next year across all major economic indicators. Even so, the state is forecast to outperform the national economy. However, downside risks to the forecast remain a key consideration, with uncertainty created by the war in Ukraine and supply-chain issues.

Arizona economy developments

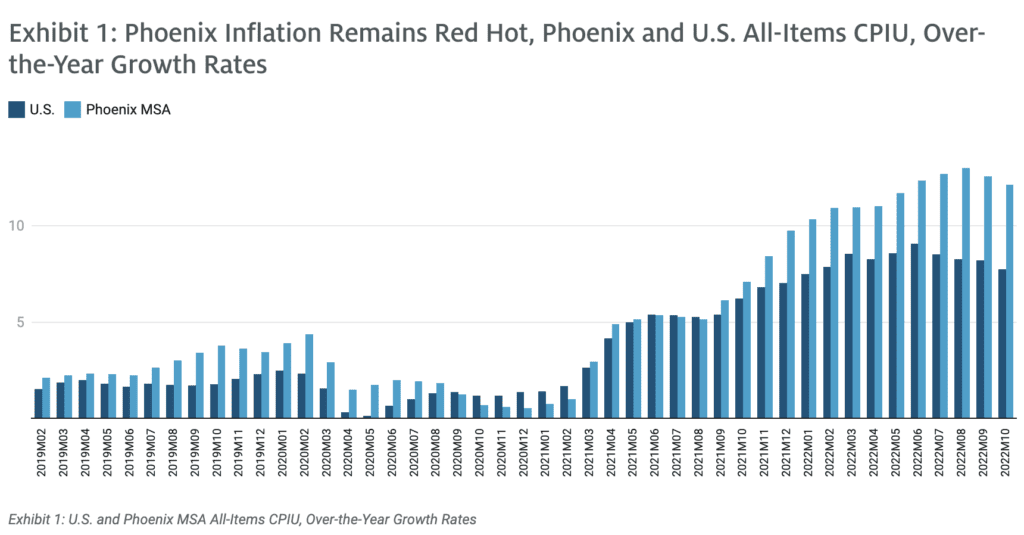

Inflation remains a key concern, with prices rising much faster in the Phoenix MSA than nationally. In October, U.S. inflation measured by the all-items Consumer Price Index for All Urban Consumers (CPIU) was 7.7% over the year. Prices in the Phoenix MSA rose even faster in October, up 12.1% over the year (Exhibit 1). Price increases in commodities have moderated slightly from their summer peak, but services inflation (which includes housing) continues at a very rapid pace, particularly in Phoenix.

Exhibit 1: Phoenix Inflation Remains Red Hot, Phoenix and U.S. All-Items CPIU, Over-the-Year Growth Rates

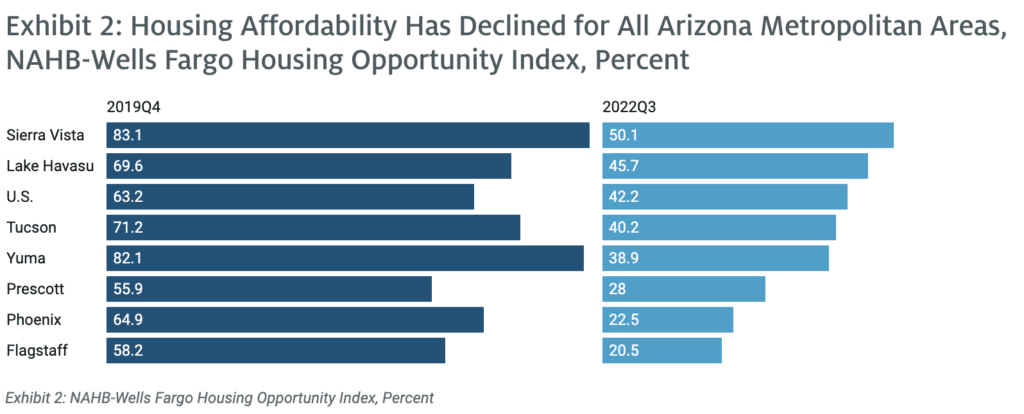

Skyrocketing house prices have driven inflation in Phoenix well above the national average. They have also pushed housing affordability to very low levels in the third quarter of 2022. According to data from the NAHB-Wells Fargo Housing Opportunity Index, 22.5% of homes sold in the Phoenix MSA in the third quarter were affordable to a family making the median income (Exhibit 2). That was up slightly from 22.3% in the second quarter, but well below the national average of 42.2% and miles below Phoenix affordability in the fourth quarter of 2019 (64.9%).

Exhibit 2: Housing Affordability Has Declined for All Arizona Metropolitan Areas, NAHB-Wells Fargo Housing Opportunity Index, Percent

Compared to February 2020, Arizona jobs were up by 103,800 in October. During that period, the strongest job gains were in trade, transportation and utilities, education and health services, manufacturing, financial activities, construction, and professional and business services. Jobs in government and leisure and hospitality remained well below their February 2020 level in October.

The state’s seasonally-adjusted unemployment rate ticked up from 3.7% in September to 3.9% in October. That was slightly above the U.S. rate of 3.7%. Even so, the state’s labor market remains very tight.

As of October, Tucson replaced 95.4% of the jobs lost during the first two months of the pandemic. Since February 2020, trade, transportation, and utilities has generated by far the most jobs, followed by manufacturing and education and health services. In contrast, professional and business services has lost the most, followed by government, leisure and hospitality, information. Jobs in other services, construction, and natural resources and mining are close to their February 2020 level.

Tight labor markets have driven strong wage gains. One key measure of wage/price pressures is the Employment Cost Index (ECI) from the U.S. Bureau of Labor Statistics. Overall compensation growth in the Phoenix MSA was 5.5% over the year in the third quarter, just above the U.S. at 5.2%. Even so, compensation growth was well below Phoenix inflation in the third quarter.

Arizona Outlook

The outlook for Arizona, Phoenix, and Tucson depends in part on national and global economic events. The baseline forecast from IHS Markit calls for U.S. real GDP to increase by 1.7% in 2022 (annual average basis) before dropping by 0.5% in 2023. Growth rebounds to 1.3% in 2024 and again to 2.0% in 2025. On a quarterly basis, the forecast calls for real GDP to decline from the fourth quarter of 2022 through the second quarter of 2023. The peak-to-trough decline is 1.1%, which would be similar to the (relatively mild) early 1990s recession.

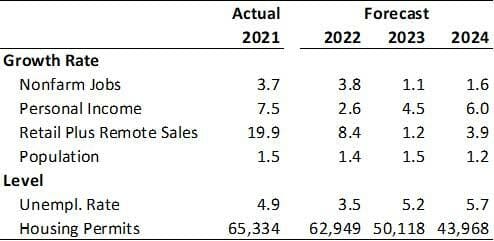

If the U.S. economy falls into recession, it will take the wind out of Arizona’s sails. As Exhibit 3 shows, Arizona job growth decelerates from 3.8% in 2022 to 1.1% in 2023 and 1.6% in 2024.

Exhibit 3: Arizona Outlook Summary

Slowing job gains drive the state’s unemployment rate up from 3.5% in 2022 to 5.2% in 2023 and 5.7% in 2024.

Nominal personal income growth is forecast to decelerate from 7.5% in 2021 to 2.6% in 2022, as federal pandemic-related income support ends. Income growth rebounds to a modest 4.5% in 2023 as wage gains decelerate with loosening labor markets.

Growth in nominal retail sales (including remote sales) decelerates from 19.9% in 2021 to 8.4% in 2022 and then to 1.2% in 2023 as negative real income growth, wealth effects (declining stock and real estate values), and reduced consumer confidence take their toll on consumers.

Population growth cycles up and down modestly in the near term, reflecting residual effects of the pandemic on net migration and natural increase (births minus deaths).

Skyrocketing mortgage rates, plummeting housing affordability, and slowing population growth combine to drive housing permit activity down from 65,334 in 2021 to 43,968 in 2024.

Risks to the Outlook

With this forecast, the U.S. baseline (most likely) scenario includes a mild recession. The pessimistic scenario assumes a deeper downturn while the optimistic scenario assumes that performance is somewhat better. The baseline scenario is assigned a 55% probability, while the pessimistic scenario is assigned 30%. The remaining 15% is assigned to the optimistic scenario.

Those assumptions translate into something similar for Arizona. While there are modest quarterly job losses in the baseline and pessimistic scenarios, the downturn is expected to be less severe in Arizona than nationally. In particular, the baseline forecast calls for peak-to-trough job loss in Arizona to reach 0.5%. The U.S. forecast calls for national job loss to hit 2.1%.

George W. Hammond, Ph.D., is the director and research professor at the Economic and Business Research Center (EBRC).