Following two months of year-over-year declines, home prices rose in August (+0.7%) as the number of homes on the market decreased for the second month in a row, down -7.9% year-over-year, according to the Realtor.com August Monthly Housing Trends Report released today. Active inventory remained -47.8% below typical 2017 to 2019 levels, although an unseasonable increase in newly listed homes from July to August (+3.5%) this year provides more options for home shoppers as the fall buying season approaches. In Phoenix-Mesa-Chandler, the median listing price is $538,000, a 7.6% year-over-year increase.

MORE NEWS: Arizona housing affordability takes another tumble

“While the uptick in new listings is good news for home shoppers, inventory remains persistently low, even with record-high mortgage rates putting a damper on demand,” said Danielle Hale, Chief Economist for Realtor.com®. “The inventory crunch continues to put upward pressure on home prices, amplifying affordability concerns and shutting some potential buyers out of the market. However, we anticipate mortgage rates will gradually ease through the end of the year and, despite this month’s bump in home prices, we’ll be unlikely to see a new price peak this year.”

What it means for homebuyers, sellers, and the housing market

Although home sellers were less active in August compared to last year, the increase in newly listed homes for sale from July to August creates a nice boost for shoppers heading into fall, which is typically the best time to buy a home. Homeowners who have been on the fence about selling will likely find eager buyers looking for fresh listings.

“As fall buying activity heats up, the newly available homes for sale aren’t likely to remain on the market long, so sellers and hopeful homebuyers will need to be prepared to move quickly,” said Realtor.com® Executive News Editor Clare Trapasso. “Home shoppers can save searches on Realtor.com® to receive real-time alerts, receive mortgage pre-approvals, and pore over their budgets to determine what they can realistically afford with today’s higher mortgage rates.”

Affordability remains a significant concern. Although sales of new homes are on the rise, construction activity isn’t sufficiently robust to offset the inventory shortage and ease prices, which are up nearly 38% from August 2019 levels. Additionally, elevated mortgage rates have raised the monthly financing cost of the average home by about $417, up 21.7% from August 2022. This greatly exceeds both wage growth (4.4%) and inflation (3.2%).

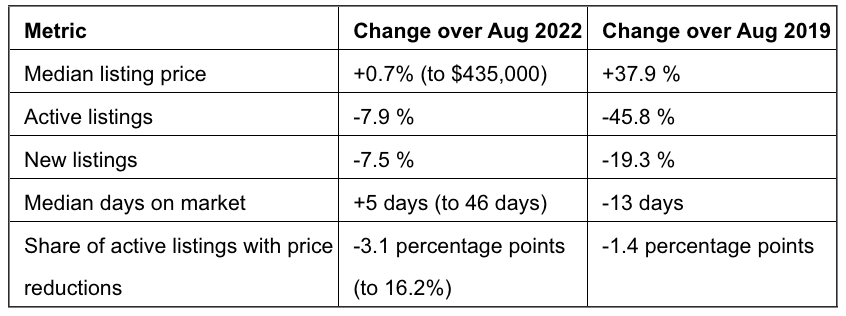

August 2023 Housing Metrics – National

Year over year home prices rise in August after two months of annual declines

In August, national home listing prices rose slightly compared to last year, ending a two-month streak of year-over-year price declines in June and July, buoyed by a scarce inventory of homes for sale across the country. Despite listing prices being slightly higher than in August of last year, the median list price is unlikely to surpass last year’s record peak of $449,000 in June 2022 as we head into the fall months and when home prices typically see a slight seasonal decline.

- The U.S. median list price fell to $435,000 in August, down from $440,000 in July, but is up slightly (+0.7%) from August of last year.

- While all regions saw listing prices in larger metros increase on average, Northeastern metros had the highest growth rate in active listing prices, with an average increase of 9.7% over the past year.

- Among the 50 largest U.S. metros, only 7 saw their median list price decline compared with this time last year, down from 12 last month. The greatest year-over-year price declines were seen in Raleigh (-4.6%) and Las Vegas (-2.8%). Larger southern metros saw the lowest listing price growth rate among the regions (3.2%).

- Nationally, the share of homes with price reductions decreased from 19.3% in August of last year to 16.2% this year, and remains below typical levels seen in 2017 to 2019.

- Among the 50 largest metros, the largest increases in the percentage of homes with price reductions compared to last year were in San Antonio (+3.9 percentage points), Memphis (+3.7), and Oklahoma City (+1.9).

Newly listed homes improve from July, but inventory crunch continues: While the market saw an unusual bump in newly listed homes for sale between July and August this year, the overall number of homes actively for sale shrank for the second consecutive month, reversing the consistent growth trajectory seen since April 2022. Some of this drop can be attributed to an off-season surge in inventory during a market slowdown last summer. Although active inventory still remains below typical pre-pandemic levels seen between 2017 and 2019, the modest rise in new homes listed for sale this summer could give buyers grappling with affordability issues more options.

- Nationally, active inventory shrank -7.9% year over year in August compared to last year. On average, active inventory in August was -47.8% below typical 2017–2019 levels.

- Pending listings, or homes under contract, declined by 11.5% compared to the same time last year, which is slightly smaller than July’s 12.6% decline and much improved from December’s peak decline (-36.9% year over year).

- Newly listed homes were 7.5% below last year’s levels, but this rate of decline is much improved from a decline of 20.8% in July. Newly listed homes increased by 3.5% from July to August.

- In all regions, the inventory of homes actively for sale was down 30%–60% from pre-pandemic levels. Inventory declined least in the South, by 1.5% compared to the same time last year, followed by a decline of 13.5% in the Midwest, 19.3% in the Northeast, and 31.5% in the West.

- In August, only Milwaukee (+6.8%) and Jacksonville (+4.0%) saw new listings increase over the same time last year. Declines in new listings were greatest in Nashville (-27.2%) Cincinnati (-25.0%) and Seattle (-24.7%).

As inventory shrinks, homes in several large markets sell faster compared to last year: The time homes spend on the market is approaching last year’s quicker figures, with buyers again vying for fewer available options than the prior year in most parts of the country. Should this pattern continue, by the coming month homes in every region except the South are likely to sell faster than they did during the same period last year.

- In August, the typical home spent 46 days on the market, 5 days longer than this time last year, but 13 fewer days than they did on average from August 2017–2019.

- Time on market increased in August compared to last year in 35 of the 50 largest metro areas. Larger metros in the South saw the greatest increase (+6 days), followed by the Northeast (+2 days), Midwest (+1 day) and West (+0 days).

- At the market level, time on market increased the most in Austin and New Orleans (+15 days), as well as in Miami (+13 days).